Accounting for Long-Term Assets and Intangible Assets

– Account for the sale of long-term assets: At a Gain, At a Loss, or When we trade in an old asset and purchase a new asset

– Account for impairment of long-term assets: When future cash flows

– Long-term assets are assets that help generate revenue. Long-term assets are classified into two major categories:

– Tangible assets: Assets in this category include land, land improvements, buildings, equipment, and natural resources.

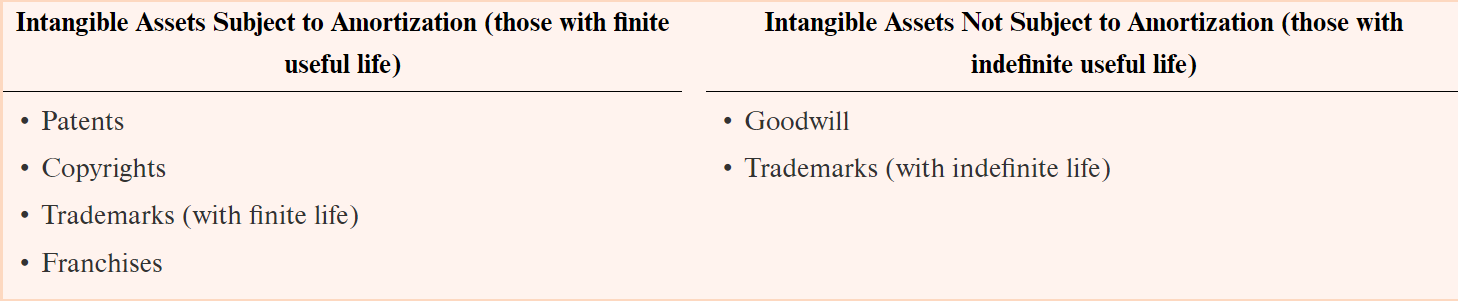

– Intangible assets: Assets in this category include patents, trademarks, copyrights, franchises, and goodwill. We distinguish these assets from property, plant, and equipment by their lack of physical substance. The evidence of their existence often is based on a legal contract.

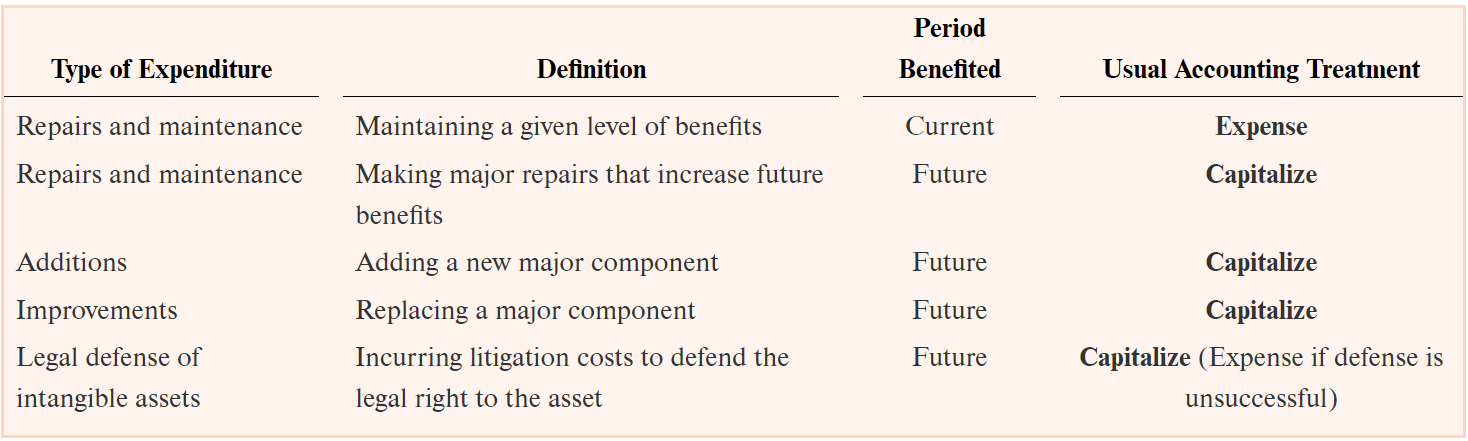

– Capitalize: This word means that we record an expenditure of cash as an asset (not an expense) *(no change in total assets)*

– Assets are recorded at: Cost of Asset + All expenditures necessary to get it ready for use

– Land: land used for operations (factory sites, retail operations, corporate HQ)

– Land improvements: include parking lots, sidewalks, driveways, landscaping, lighting systems, fences, etc. (current year taxes are not capitalized)

– As with land, costs to capitalize in the Buildings account will include purchase price, commissions paid, architectural fees (for new construction), remodeling/upfit costs, etc.

– Costs to capitalize Equipment will likely include purchase price, sales taxes, shipping and delivery fees, installation costs, etc.

– Recurring costs are not part of preparing the equipment for use so they are not capitalized as part of the Equipment account. Examples would be insurance, vehicle taxes, or normal maintenance costs.

– We may purchase a “basket” of assets for one price. The best example is a factory that consists of land, buildings, and equipment.

– Depletion: allocation of the cost of a natural resource over its service life

– Intangible Assets: No physical substance – these assets convey valuable rights to owners through what they allow the owner to do (or prevent others from doing).

Acquired in two ways: 1. Purchase from others (record purchase price as the capitalized amount), 2. Create internally (typically very little (if any) is capitalized in these situations)

– Patents: exclusive right to manufacture a product or to use its process

When purchased: capitalized for the purchase price plus any legal and filing fees related to change in ownership

When internally developed: capitalized for legal and filing fees only

– Copyrights: the exclusive right of protection given to the creator of a published work

– Trademarks: Word, slogan, or symbol that distinctively identifies a company, product, or service. Capitalized for legal, registration, and design fees.

– Franchises: Local outlets that pay for the exclusive right to use the franchisor’s name and to sell its products. Capitalized for initial fee.

– Goodwill: Only recognized when one company buys another company.

Represents the additional value of a company as a whole, over and above the value of its individual net assets.

Recorded amount equals: Purchase Price – Fair value of the net assets acquired

– We capitalize an expenditure of an asset if it increases future benefits.

– We expense an expenditure if it benefits only the current period.

– Depreciation in accounting is the process of allocating to an expense the cost of an asset over its service life.

– Accumulated depreciation: A contra-asset account (an asset account with a normal credit balance) that represents the total depreciation taken to date

– Service life: The time period over which the company expects to receive benefits from the asset before disposing of it

– Residual value: Also know as salvage value. This is the amount the company expects to receive from selling the asset at the end of its service life (often is zero—but not always)

– These are the three methods you need to know—there are others but they are related to these three types:

Straight-line method – depreciation expense is equal each year

Double Declining-balance method – depreciation expense will decline over time

Activity-based method – depreciation is based on actual usage (e.g., operating hours, miles driven, or units produced)

– Allocating the cost of intangible assets to expense is called amortization.

– A retirement is when a long-term asset is no longer useful but cannot be sold.

– An exchange occurs when two companies trade assets. In a trade, we often use cash to make up for any difference in fair value between the assets.

– Impairment: occurs when the future cash flows (future benefits) generated for a long-term asset fall below its book value

– With basket purchases, find percentages for each asset by adding all assets and seeing what % each holds of the total then take answer choices with the total amount paid and multiply by % of whichever asset you need to find to check if it matches the # given paid for given asset in question

– For goodwill, you take the fair value of assets and subtract off the liabilities then take the purchase price and subtract the purchase price – your estimated fair value after subtracting

– Depreciable Cost = Cost – Residual value

– Straight-Line Rate = 1 / Estimated Useful Life

– Double-Declining Depreciation Balance Rate = 2 / Estimated Useful Life

– Book Value = Cost – Accumulated Depreciation

– Total depreciation expense over the life of the asset cannot exceed the depreciable amount

– When the Book Value = Residual Value THEN the depreciation process stops

– A line of credit is an informal agreement that permits a company to borrow up to a prearranged limit without having to follow formal loan procedures and prepare paperwork.

– If a company borrows from another company rather than from a bank, the note is referred to as commercial paper. The recording for commercial paper is exactly the same as the recording for notes payable described earlier

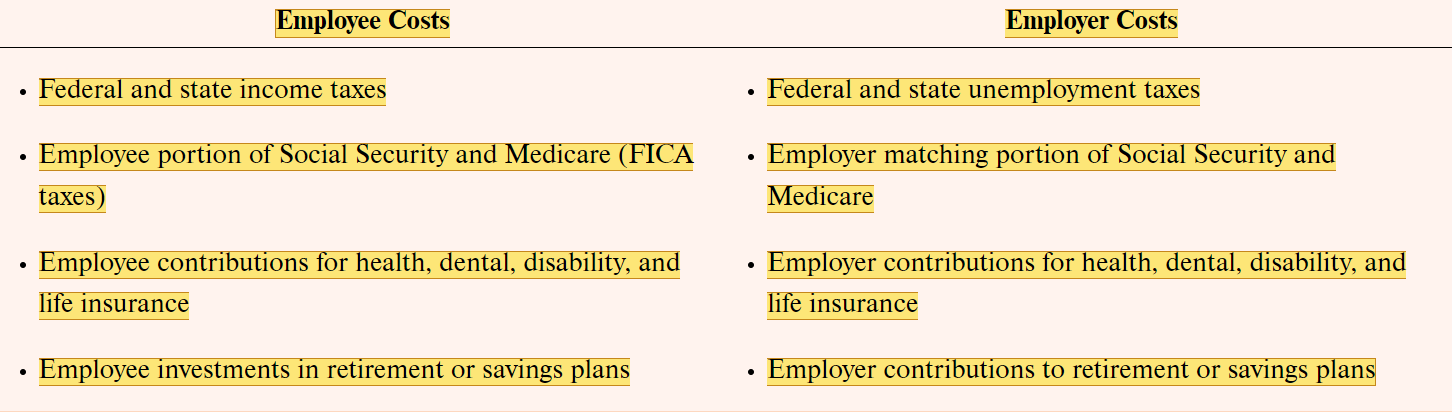

– Employee Payroll Costs:

Federal and State income taxes withheld

FICA taxes

7.65% (6.2% + 1.45%)

Collectively, Social Security and Medicare taxes

Employees may opt to have additional amounts withheld from their paychecks for Union Dues, Retirement Acct Contributions, insurance, Parking, etc.

– Employer Payroll Costs:

Salaries earned by employees

Additional (matching) FICA tax on behalf of the employee

Employers also pay federal and state unemployment taxes on behalf of its employees (FUTA and SUTA)

Fringe benefits: Additional employee benefits paid for by the employer (e.g., Health Insurance, Retirement Plans)

Other Current Liabilities:

– Deferred revenues: liability account used to record cash received in advance of the sale or service

– Sales tax payable: collected from customers by the seller and remitted to City and/or State

– Current portion of long-term debt: debt that will be paid within the next year

– Employee salaries are reduced by withholdings for federal and state income taxes, FICA taxes, and the employee portion of insurance and retirement contributions. The employer, too, incurs additional payroll expenses for unemployment taxes, the employer portion of FICA taxes, and employer insurance and retirement contributions.

– If the likelihood of payment is probable and if one amount within a range appears more likely, we record that amount. When no amount within the range appears more likely than others, we record the minimum amount and disclose the range of potential loss.

– If the likelihood of payment is only reasonably possible rather than probable, we record no entry but make full disclosure in a note to the financial statements to describe the contingency.

– Finally, if the likelihood of payment is remote, disclosure usually is not required.

– Warranties: the most common example of contingent liabilities

Warranties help increase sales

Warranty expense is recorded in the same accounting period as the sale (matching principle in action)

– To record estimated warranty amount:

Debit Warrenty Expense

Credit Warrenty Liability

– Then to record actual warranty expenditures:

Debit Warrenty Liability

Credit Cash

– Contingent Gains: an existing uncertain situation that might result in a gain

Not recorded until the gain is certain

– Liquidity Analysis: refers to having sufficient cash or other current assets to pay currently maturing debts

– Working Capital: Working Capital = Current Assests – Current Liabilties

– Current Ratio: Ratio of 1.0 or higher often reflects an acceptable level of liquidity; Higher the current ratio, the greater the company’s liquidity

– Acid-Test Ratio: Quick assets are readily convertible into cash (excludes inventory and prepaid expenses)

– Time Value of Money: interest causes the value of money received today to be greater than the value of that same amount of money received in the future.

– Simple interest: interest earned on the initial investment only

– Compound interest: interest earned on the initial investment and on previous earned (but unpaid) interest

– Annuity: equally sized payments within a given time period

– Table 1 is used when given present value with the rate and # of years in order to find future value (How much will I have after _ number of years?)

– Table 2 is used when given desired future value with the rate and # of years in order to find present value (How much do I need to invest today?)

Future Value of Annuity – payments made at the end of year year (ordinary annuity)

– Table 3 is used when payments are spaced out in time in order to find out how much you’ll have at the end of the time period (Key-word: each year)

Find out how many periods (if quarterly and 3 years that 12 periods), then divide interest rate by how many years to find the correct value on table to multiply by payment amount

Present Value of Annuity: each annuity payment represents a single future amount

– Table 4 is used to find the initial investment given the final annuity amounts (Key-words: payments of, real value today) (finds individual payments)