Accounting Concepts and Transactions

Bank’s Cash Balance: Company’s Cash Balance: – Gross profit = net sales revenue – cost of goods sold

+ Deposits outstanding + Notes received by bank – Initial Inventory + Purchased Inventory – Ending Inventory = COGS

– Checks outstanding + Interest received

– Unrecorded payments

– NSF checks from customers

– Bank service dee

+/- bank errors +/- company errors

Record items that increase cash by debiting cash and crediting notes/interest.

Record items that decrease cash by debiting expenses/services/receivables from NSF checks and crediting cash. (No adjusting entries for the bank!)

– Sales Returns: Seller issues a full refund; Customer returns the product

– Sales Allowance: Seller reduced the customer’s balance owed partially; Customer does not return product

–Sales Discounts: intended to provide an incentive to a customer for quick payment.

Purchase discounts are when a company is granted a discount

Sales discounts are when a company grants the buyer

– Net Sales (aka net revenues): A company’s total sales less any discounts, returns, & allowances

Net Sales = Sales – Sales Discounts – Sales Returns & Allowances

–Weighted-average cost (WAC): Calculated as: Cost of goods available for sale / Number of units available 4 sale

– Ending Inventory with WAC→ take the total cost of goods & divide by # of units to find the average value of a unit, then, take the total # of units & subtract units sold to find the ending units, then multiply the ending units by the average value of units to find ending inventory value

– If cost is lower than NRV, no adjusting entry is needed. If NRV is lower than cost, adjusting entry is required debiting COGS & crediting inventory.

– Ending Inventory you would multiply your quantity by the LOWEST # either NRV or Cost.

– When calculating the total AFUA and it already has a normal credit balance, you adjust accordingly through the percentage then debit bad debt expense to get the desired total and credit AFUA (if debit balance then add) (always looking for desired credit balance AFTER adjustment)

– Beginning AR balance + Credit Sales – Collections – Specific Write-Offs = Ending AR balance

– Account for impairment of long-term assets: When future cash flows

– With basket purchases, find percentages for each asset by adding all assets and seeing what % each holds of the total then take answer choices with the total amount paid and multiply by % of whichever asset you need to find to check if it matches the # given paid for given asset in question

– For goodwill, you take the fair value of assets and subtract off the liabilities then take the purchase price and subtract the purchase price – your estimated fair value after subtracting

– When inventory costs are rising, FIFO results in: (& if inventory costs falling then LIFO is all the same)

1. Higher reported amount for inventory in the balance sheet

2. Higher reported gross profits in the income statement

– Depreciable Cost = Cost – Residual value

– Straight-Line Rate = 1 / Estimated Useful Life

– Double-Declining Depreciation Balance Rate = 2 / Estimated Useful Life

– Book Value = Cost – Accumulated Depreciation

– To record estimated warranty amount:

Debit Warrenty Expense

Credit Warrenty Liability

– Then to record actual warranty expenditures:

Debit Warrenty Liability

Credit Cash

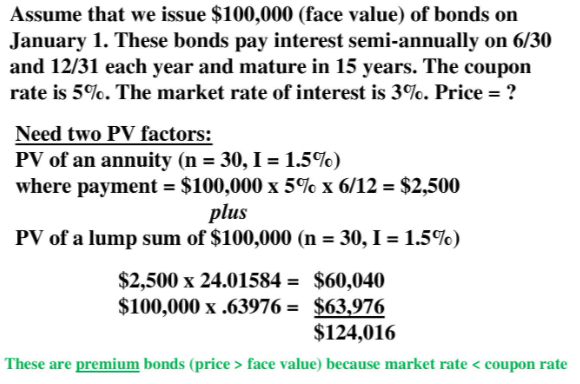

– Table 1 is used when given present value with the rate and # of years in order to find future value (How much will I have after _ number of years?)

– Table 2 is used when given desired future value with the rate and # of years in order to find present value (How much do I need to invest today?)

Future Value of Annuity – payments made at the end of year year (ordinary annuity)

– Table 3 is used when payments are spaced out in time in order to find out how much you’ll have at the end of the time period (Key-word: each year)

Find out how many periods (if quarterly and 3 years that 12 periods), then divide interest rate by how many years to find the correct value on table to multiply by payment amount

Present Value of Annuity: each annuity payment represents a single future amount

– Table 4 is used to find the initial investment given the final annuity amounts (Key-words: payments of, real value today) (finds individual payments)

FV = PV x Table 1 Factor PV = FV x Table 2 Factor FVA = PMT x Table 3 factor PVA = PMT x Table 4 Factor

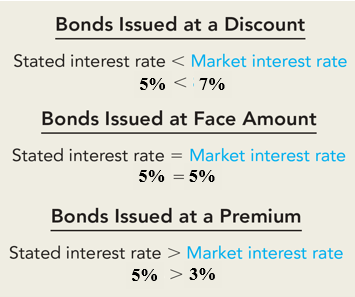

– Unsecured bonds – no collateral exists. (Unsecured bonds are much more common than secured bonds)p

– Term bonds – All of the bonds in a specific issuance mature at the same time (for example, issue 1,000 bonds, and all 1,000 mature in ten years)

– Serial bonds – These types of bonds mature serially (in installments).

– Callable bonds – These may be bought back by the issuer before the maturity date at a predetermined price

– Convertible bonds – These may be converted to common stock by the investor (if they want to convert them—they don’t have to)

(Interest expense = carrying value x market rate, while the cash paid for interest is the face amount x the stated rate)

– (Always use the market rate from the issue date to find the correct factors from tables)

– (Use the discount rate to find the # you credit cash after the plug for a discount on B/P; coupon rate is used to find the basic payment over the period without using table factor, then use that number and multiply by the factor to find total amount)

– (Use the stated rate to calculate the interest payment each period, but use the market rate to calculate the present value of the cash flows.)

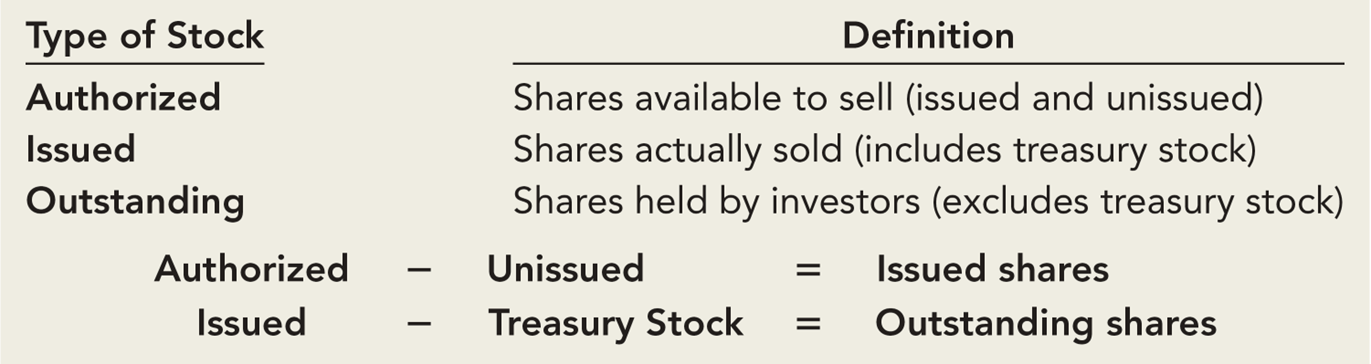

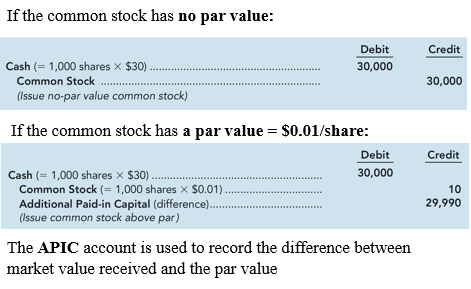

– Par Value: Legal capital per share of stock that’s assigned when the corporation is first established. Sometimes referred to as stated value. Has no relationship to the market value today.

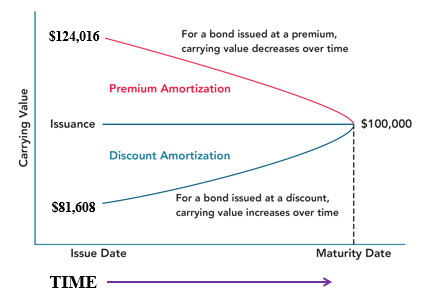

– For bonds issued at a discount or at a premium to face value, in each successive entry to recognize interest expense, both the discount and the premium amortizations will be higher.

– A company declares and distributes a 30% common stock dividend to common stockholders. By how much will the retained earnings balance be affected as a result of this transaction (note: consider any effects associated with closing entries)?

Large stock dividends are valued at the par value of the shares issued. This would be the amount the retained earnings account would be reduced by.

– $24 million liability retired for $27 million = $3 million loss (Carrying Value – Book Value)

– $112,000 CV x .07 x 6/12 = $3,920 The entry is: (Selling Price x Market Rate x Period of Time) — to recognize interest expense on a bond

Interest Expense 3920

Premium on B/P 580

Cash 4500

–

(issuance of CS with $1 par value and $10 per share)

(issuance of CS with $1 par value and $10 per share)

– Net Accounts Receivable Expected to Collect = Ending Accounts Receivable Balance – Allowance for Uncollectible Account